A message arrives in your inbox or mailbox saying you have been pre-approved for a credit card or loan. It feels reassuring and even validating. Many Canadians interpret this as a guarantee that the funds are already theirs. Others assume it means the lender has fully reviewed their financial situation.

In reality, the difference between pre-approved vs pre-selected offers is often misunderstood, and that misunderstanding can lead to poor borrowing decisions. These terms are used across the credit industry, including credit cards, personal loans, and even payday loans, yet they do not carry the same meaning.

Understanding what these labels actually represent gives you control. It allows you to make borrowing decisions based on facts instead of assumptions, and to recognize when an offer is truly meaningful versus when it is simply marketing.

Definition of Pre-Qualification and Pre-approval: The First Layer of Screening

Pre-qualification and pre-approval are often used interchangeably in conversation, but they represent different stages of the lending process. Both are designed to give lenders and borrowers a preliminary sense of eligibility, yet the depth of review varies significantly.

Pre-qualification is usually the earliest step. At this stage, lenders review basic financial information such as income, employment, and general financial standing. This review often relies on self reported information and may include only a soft credit inquiry or none at all. The result is an estimate, not a commitment, of what you may qualify for.

Pre-approval involves a more detailed review. The lender typically evaluates your credit profile more closely and may perform a soft credit check to assess your borrowing history. This process gives the lender greater confidence in extending a conditional offer. Many lenders offering online payday loans use pre-approval to provide borrowers with faster decisions while still maintaining responsible screening practices.

Academic research has shown that lenders rely on predictive credit models and financial data analysis to assess borrower eligibility during these early screening stages, helping determine risk before issuing formal approval offers. While neither stage guarantees final approval, pre-approval carries significantly more weight because it reflects deeper financial verification.

Pre-Approved Meaning: A Conditional Yes Based on Real Data

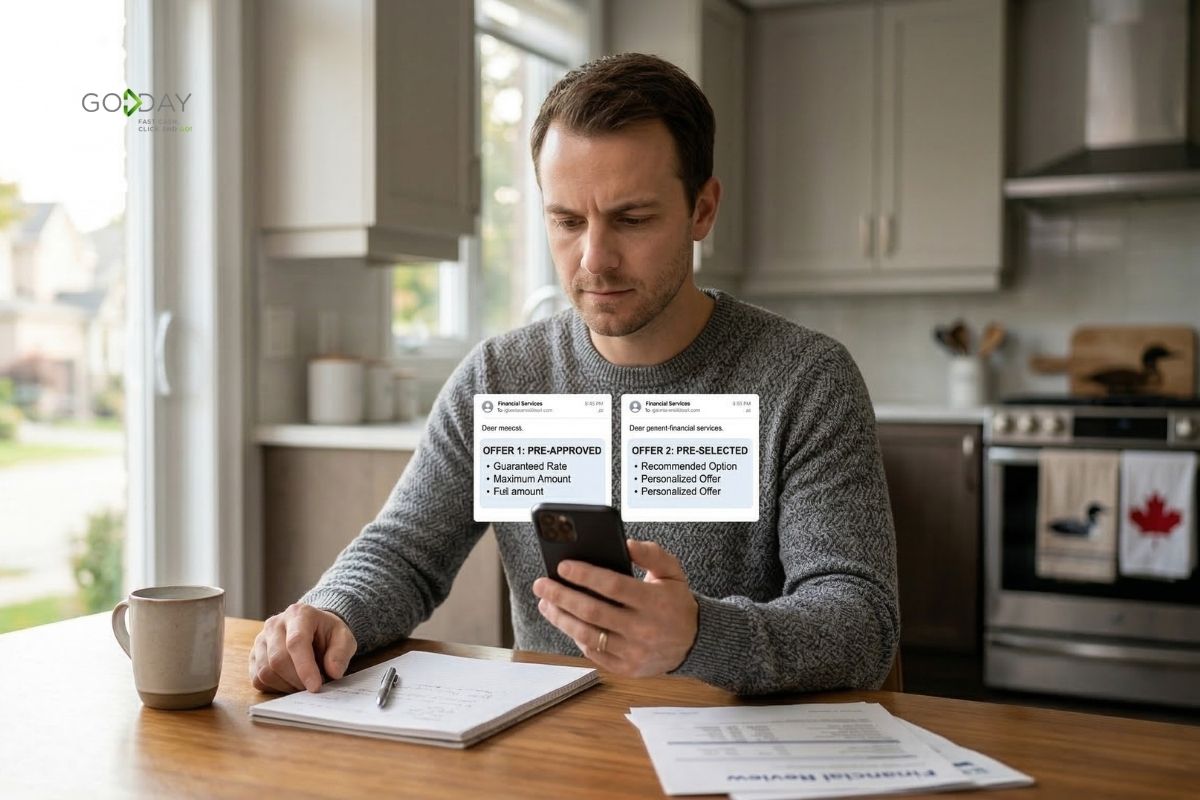

When you receive a pre-approved offer, it usually means the lender has already evaluated your financial profile and determined that you meet their basic lending criteria. In many cases, the offer includes specific details such as a loan amount, credit limit, or estimated terms. This level of specificity reflects a higher degree of certainty compared to general marketing offers.

However, pre-approval is still conditional. The lender will confirm your information during the formal application process, including verifying your income, identity, and overall financial stability. If your situation has changed since the pre-approval was issued, the final terms or approval itself could also change.

This process is common across many forms of credit, including instant approval loans, where lenders combine pre-screening with fast verification to deliver quicker lending decisions. The key advantage of pre-approval is that it reduces uncertainty, allowing borrowers to move forward with greater confidence while still understanding that the process is not fully complete.

The Government of Canada also notes that credit offers should always be reviewed carefully, since final approval depends on full verification and individual financial circumstances.

Pre-Selected Meaning: A Marketing Signal, Not a Credit Decision

Being pre-selected is fundamentally different. It does not mean the lender has confirmed your eligibility. Instead, it means you fit a general profile that the lender considers desirable based on marketing data, demographic information, or limited financial indicators.

Pre-selected offers are designed to encourage you to apply, but they do not include guaranteed approval or confirmed loan terms. Once you apply, the lender will perform a full review of your credit and financial information before making a final decision. This means approval is still uncertain, and rejection is possible.

Key Differences Between Pre-Approved and Pre-Selected Offers

The most important distinction between pre-approved and pre-selected offers lies in the level of verification and certainty behind them. Pre-approved offers are based on a more detailed review of your financial profile, while pre-selected offers are based on general criteria.

Pre-approved offers typically involve:

- A review of your credit profile

- A conditional offer with specific terms

- A higher likelihood of final approval

Pre-selected offers typically involve:

- Limited initial screening

- No guaranteed approval

- A full application and credit check required

Understanding these differences helps you evaluate offers more accurately and avoid assuming approval before it is confirmed.

Impact on Credit Score and Final Approval: What Really Matters

Many borrowers worry that receiving or responding to these offers will damage their credit score. In most cases, the initial pre-qualification or pre-approval process involves a soft inquiry, which does not lower your credit score or affect your borrowing ability.

The more important factor is what happens after you accept the offer. Once you formally apply, the lender may perform a hard credit inquiry, which can cause a small and temporary decrease in your score. However, your long term credit health depends far more on repayment behavior and credit management.

The true impact of credit history comes from making payments on time, maintaining reasonable balances, and managing credit responsibly over time. According to the Government of Canada, lenders use your credit report and score to evaluate your reliability and determine approval decisions, interest rates, and borrowing limits. These factors influence your financial reputation far more than any single inquiry or offer.

Importance and Benefits of Pre-Qualification and Pre-Approval

Despite the confusion surrounding these terms, both pre-qualification and pre-approval can be valuable tools when used correctly. They allow you to explore your borrowing options without immediately committing to a full application or risking unnecessary credit checks.

These processes can help you:

- Understand what loan amounts you may qualify for

- Compare lenders more effectively

- Plan ahead for financial needs

- Avoid unnecessary hard inquiries

This is particularly useful for borrowers exploring bad credit loans in Canada, where understanding eligibility in advance can prevent unnecessary applications and protect credit health.

Government guidance also explains that improving and understanding your credit profile can help you access better borrowing opportunities and make more informed financial decisions.

Types of Loans and Credit Products Involved

Pre-approved and pre-selected offers are used across a wide range of credit products, not just credit cards. These offers can apply to personal loans, lines of credit, installment loans, and short term lending solutions.

Borrowers may also encounter these offers when exploring loan options beyond traditional banks, including alternative lenders who use modern approval models that consider multiple financial factors. These lenders may evaluate income patterns, employment stability, and banking behavior in addition to credit scores.

Understanding the type of credit involved is essential because each product carries different costs, repayment structures, and financial implications. Taking the time to review the details ensures that the offer aligns with your financial goals.

Process for Obtaining Pre-Qualification and Pre-Approval

If you want to pursue pre-qualification or pre-approval intentionally, the process is usually simple and accessible. Most lenders allow you to complete an initial screening online by providing basic personal and financial information.

This information typically includes your income, employment status, and identity verification. Many lenders use soft credit inquiries at this stage, which allows you to explore options without affecting your credit score. This process gives you a clearer understanding of what may be available before committing to a full application.

Educational resources from the Government of Canada also explain that reviewing your credit and understanding credit and lending requirements in advance helps consumers make informed borrowing decisions.

By using pre-qualification strategically, borrowers can compare offers and select credit solutions that match their needs without unnecessary risk.

Post Pre-Approval Steps and Next Actions

Receiving a pre-approved offer should always be followed by careful evaluation. Even if the lender has indicated approval, it is important to review the terms, interest rates, and repayment schedule to ensure the credit fits comfortably within your budget.

Borrowing should always serve a clear purpose, whether it is managing an unexpected expense, consolidating debt, or improving financial flexibility. Accepting credit without a clear plan can create unnecessary financial strain.

Taking time to evaluate the offer ensures that the decision supports your long term financial health instead of compromising it.

Opting Out and Managing Loan Offers

If you receive frequent pre-selected or pre-approved offers, it is important to remember that you are not obligated to accept them. You can ignore offers that do not align with your needs or opt out of promotional communications if they become overwhelming. This applies to all types of credit, including credit cards, personal loans, and payday loans, which are often marketed through pre-screened offers.

Managing these offers helps you stay focused on financial decisions that truly matter. It also reinforces the principle that borrowing should always be intentional rather than reactive.

Financial confidence comes from making informed choices, not from accepting every offer that appears in your inbox.

Making Smarter Borrowing Decisions with Confidence

Ultimately, the difference between pre-approved and pre-selected comes down to understanding how much certainty exists behind the offer. Pre-approval reflects a deeper review and greater likelihood of approval, while pre-selection represents an invitation to apply rather than a confirmed decision.

Neither label should replace thoughtful evaluation. Borrowers should always consider their financial situation, repayment ability, and long term goals before accepting any form of credit.

At GoDay, we believe Canadians deserve transparency and clarity when exploring borrowing options. When you understand the true meaning behind these offers, you gain the ability to make decisions that support your financial stability instead of undermining it.

Because in the end, the strongest financial position is not defined by the offers you receive. It is defined by the choices you make.