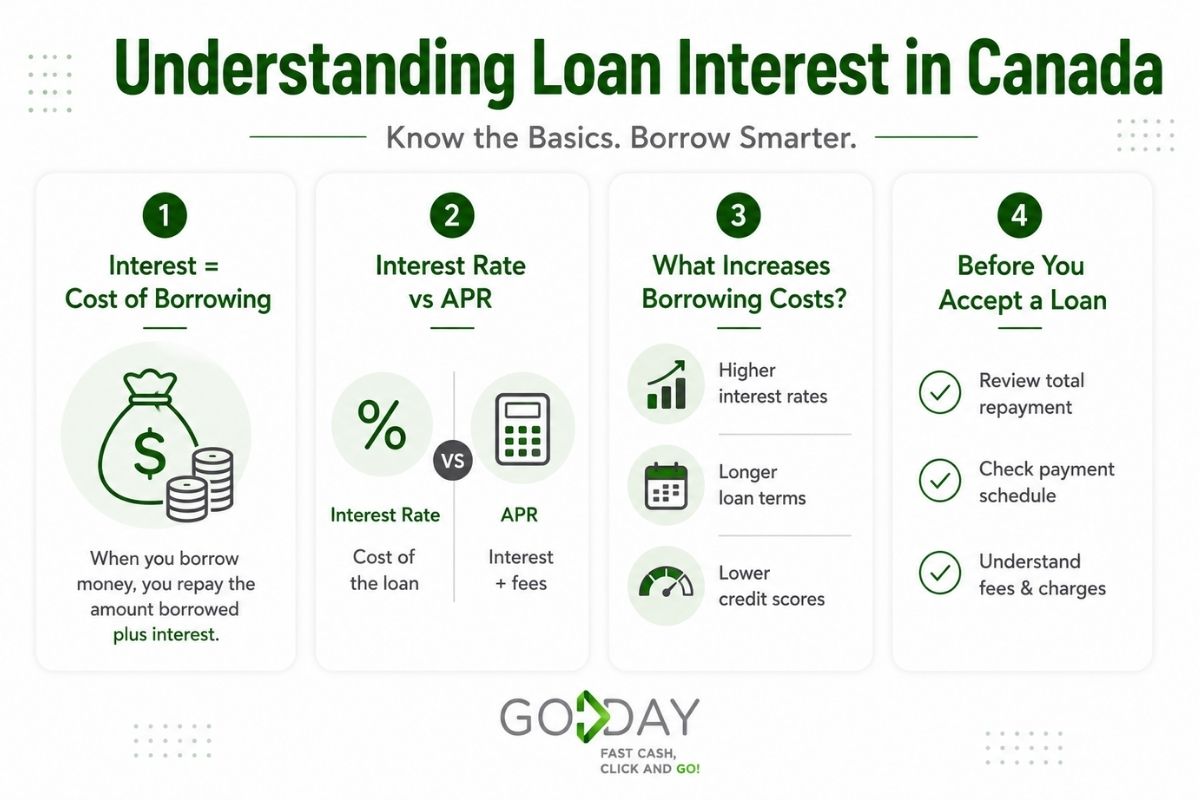

Loan interest is the cost of borrowing money. It is the amount a lender charges in exchange for giving you access to funds now, with repayment scheduled for a later date. In Canada, interest affects how much you repay on personal loans, mortgages, credit cards, lines of credit, installment loans, and other borrowing products.

Understanding how loan interest works can help borrowers make better financial decisions. Even a small difference in interest rates, repayment terms, or fees can change the total cost of borrowing over time.

For Canadians navigating changing borrowing costs, the Financial Consumer Agency of Canada’s guide to managing money during rising interest rates explains how higher rates can affect loan affordability, repayment pressure, and monthly budgeting decisions.

At GoDay, we believe borrowing should feel clear, transparent, and manageable. Whether someone is comparing long-term financing or exploring short-term support, understanding loan interest is an important first step.

What You’ll Learn

- What loan interest means and why lenders charge it

- The difference between simple and compound interest

- How lenders calculate interest on loans

- APR vs interest rate Canada borrowers should understand

- How fixed and variable interest rates work

- Why credit history can affect borrowing costs

- How loan terms influence total repayment

- What to review before accepting a loan

- How responsible borrowing can support short-term financial needs

The Basics: What Is Loan Interest?

Interest is the price you pay to borrow money. When you take out a loan, you agree to repay the original amount borrowed, known as the principal, plus interest. For example, if you borrow $1,000 and repay $1,100, the extra $100 represents the borrowing cost.

This is the foundation of understanding loan interest. The amount you pay depends on several factors, including the loan amount, interest rate, repayment term, lender fees, and how the interest is calculated.

Many Canadians researching payday loans online are not just looking for fast access to funds. They are also trying to understand what repayment will look like and how borrowing costs fit into their current financial situation.

Simple Interest vs Compound Interest

There are two common types of interest borrowers should understand: simple interest and compound interest.

Simple interest is calculated only on the original loan amount. If you borrow $1,000 at a 10% simple annual interest rate, the yearly interest would be $100.

Compound interest is calculated on both the original amount and any accumulated interest. This means the balance can grow faster over time, especially when payments are delayed or balances remain unpaid.

Compound interest can work in your favour when saving or investing. When borrowing, however, it can increase the total amount you owe if the debt is not managed carefully.

How Lenders Calculate Interest Rates

Interest rate calculations depend on the lender, the loan type, the repayment schedule, and the borrower’s financial profile.

A simplified interest formula looks like this:

Interest = Principal × Rate × Time

For example, if someone borrows $2,000 at 10% annual simple interest for one year, the interest would be $200.

However, real loan calculations may also include:

- Payment frequency

- Loan fees

- Compounding periods

- Amortization schedules

- Late payment charges

- Prepayment terms

This is why borrowers should always review the full loan agreement instead of looking only at the advertised rate.

The Office of the Superintendent of Bankruptcy Canada’s borrowing guide also recommends carefully reviewing repayment obligations, total borrowing costs, and affordability before accepting any form of credit.

APR vs Interest Rate: What Is the Difference?

The interest rate shows the cost of borrowing as a percentage of the loan amount.

APR, or annual percentage rate, gives a broader view of borrowing costs because it may include certain fees in addition to interest. This makes APR useful when comparing loan options.

For example, two loans may have the same interest rate but different APRs if one includes higher fees.

This is why APR vs interest rate Canada borrowers compare should not be treated as the same thing. The interest rate tells part of the story. APR can give a more complete picture of the annual borrowing cost.

The Financial Consumer Agency of Canada’s personal loan resource encourages borrowers to compare both APR and repayment terms carefully when evaluating loan options, since fees and timelines can significantly affect total repayment costs.

APR vs APY: Why Borrowers Confuse Them

APR and APY sound similar, but they are used differently.

APR usually applies to borrowing. It shows the yearly cost of taking out credit.

APY, or annual percentage yield, is more often used for savings accounts or investments. It reflects how much money can grow when compounding is included.

In simple terms:

- APR helps explain borrowing costs

- APY helps explain savings or investment growth

For most loan decisions, APR is the more relevant number.

How Lenders Determine Interest Rates

Lenders consider several factors when deciding what interest rate to offer. These may include:

- Credit history

- Income stability

- Existing debt

- Loan amount

- Loan term

- Type of loan

- Market conditions

- Repayment risk

A borrower with strong credit and stable income may qualify for lower rates. Someone with limited credit history or past repayment challenges may face higher borrowing costs.

Understanding how credit scores affect borrowing costs in Canada can help borrowers prepare before applying and better understand why rates vary.

Fixed vs Variable Interest Rates

A fixed interest rate stays the same throughout the loan term. This creates predictable payments and can make budgeting easier.

A variable interest rate can change over time based on market conditions or benchmark rates. Payments may rise or fall depending on how the rate changes.

Fixed rates can offer stability. Variable rates may offer flexibility, but they also create uncertainty.

The Bank of Canada’s explanation of the policy interest rate helps explain why borrowing costs can rise or fall over time, particularly for variable-rate lending products tied to broader economic conditions.

The right choice depends on the borrower’s budget, risk tolerance, and repayment timeline.

Types of Loans and Their Interest Structures

Different loan products often use different interest structures. Mortgages are usually long-term loans with amortization schedules. Credit cards typically charge compound interest on unpaid balances. Personal loans may use fixed installment payments. Lines of credit often charge interest only on the amount used.

Short-term loans are generally structured differently from mortgages or traditional long-term credit products because they are designed for smaller, more immediate borrowing needs.

For Canadians looking to apply for a fast online loan in Canada, it is important to review repayment expectations, payment timing, and total borrowing costs before accepting funds.

How Loan Terms Affect Total Repayment

The loan term is the amount of time you have to repay the loan.

A longer term may reduce individual payment amounts, but it can increase total interest paid over time. A shorter term may mean higher payments, but the total borrowing cost may be lower.

The Financial Consumer Agency of Canada’s mortgage interest guide provides a helpful breakdown of how amortization, repayment schedules, and interest structures can affect the total amount borrowers repay over time.

This is one of the most important parts of how loan interest works. The monthly payment is not the only number that matters.

Borrowers should also ask:

- How much will I repay in total?

- How often are payments due?

- Can I repay early?

- Are there extra fees?

- Does this fit my budget realistically?

The Impact of Interest Rates on Borrowers

Interest rates affect more than the final repayment amount. They can also influence monthly affordability, financial stress, and how quickly a borrower can get out of debt.

Higher interest rates can make repayment more difficult, especially when borrowers are already managing multiple expenses. Lower rates can reduce borrowing costs, but repayment habits still matter.

This is why comparing quick online borrowing solutions for Canadians should involve more than speed. Borrowers should also look at transparency, repayment structure, eligibility, and total cost.

Pros and Cons of Paying Interest

Interest is not automatically bad. It is part of how lending works. The benefit of paying interest is that it allows borrowers to access money when they need it, whether for emergencies, repairs, bills, or temporary financial gaps.

The downside is that borrowing costs can add up if loans are not managed carefully.

Responsible borrowing means:

- Borrowing only what is needed

- Understanding repayment terms

- Avoiding repeated borrowing cycles

- Reviewing total costs

- Choosing a transparent lender

Common Loan Interest Myths

Loan interest can feel confusing because many borrowers hear conflicting information.

One common myth is that the lowest monthly payment is always the best choice. In reality, lower payments over a longer period may lead to higher total interest.

Another myth is that APR and interest rate mean the same thing. They do not. Some borrowers also assume their credit score tells the full story. While credit matters, lenders may also consider income, employment, debt load, and repayment ability.

What to Review Before Accepting a Loan

Before accepting any loan, borrowers should carefully review:

- Interest rate

- APR

- Fees

- Repayment schedule

- Payment frequency

- Total repayment amount

- Late payment policies

- Early repayment options

- Lender transparency

This is especially important for first-time borrowers who may be unfamiliar with financial terms or loan agreements.

Learning what first-time borrowers should understand about loans can make borrowing feel less intimidating and help reduce rushed decisions.

Choosing a Transparent Lender Matters

A trustworthy lender should make borrowing costs easy to understand. Borrowers should not feel confused about what they owe, when payments are due, or how interest is calculated. Transparency matters because financial stress is already difficult enough without unclear terms.

Knowing what to look for in a trustworthy online lender can help Canadians compare options more confidently and avoid borrowing experiences that create more confusion than support.

Key Takeaways

- Loan interest is the cost of borrowing money

- The principal is the original amount borrowed

- Simple interest is calculated on the principal only

- Compound interest can grow faster because it includes accumulated interest

- APR gives a broader view of borrowing costs than the interest rate alone

- Fixed rates stay the same, while variable rates can change

- Credit history, income, loan type, and market conditions can affect rates

- Longer loan terms may lower payments but increase total interest

- Responsible borrowing starts with understanding total repayment costs

- Transparent lenders help borrowers make more informed financial decisions

Frequently Asked Questions

How does interest work on a loan?

Interest is the cost a lender charges for giving you access to borrowed money. You repay the original loan amount, known as the principal, plus interest. The total amount depends on the rate, repayment term, loan type, and whether the interest is simple or compound.

What is the difference between APR and interest rate?

The interest rate shows the cost of borrowing as a percentage of the loan amount. APR gives a broader picture because it may include certain fees as well as interest. When comparing loans, APR can help borrowers understand the total annual cost more clearly.

Why do different borrowers get different interest rates?

Borrowers may receive different rates because lenders assess financial risk differently. Credit history, income, employment stability, debt levels, loan amount, and repayment term can all influence the rate offered. Stronger financial profiles may qualify for lower borrowing costs.

Is a lower monthly payment always better?

Not always. A lower monthly payment can make a loan feel more affordable, but it may come with a longer repayment term. Longer terms can increase the total interest paid over time, so borrowers should review both monthly affordability and total repayment cost.

Can paying a loan off early reduce interest?

In many cases, paying a loan off early can reduce total interest because the principal balance is lowered sooner. However, borrowers should review their loan agreement first. Some lenders may have specific prepayment rules, fees, or conditions that affect early repayment.

Final Thoughts

Understanding loan interest helps borrowers make better financial decisions. Once you know how rates, APR, loan terms, credit history, and repayment structures work, it becomes easier to compare options and avoid surprises.

Loans can be useful when they are approached carefully and responsibly. The key is knowing what you are agreeing to before accepting funds.

For Canadians managing temporary financial gaps, GoDay offers flexible borrowing options with a focus on clarity, transparency, and responsible short-term financial support.