We wish more people asked what the difference is between these two types of credit inquiries, and how they affect the change in your score! Most of the time, this question comes up when a consumer is in the market for a mortgage or a new car when they begin to “shop around”. For us, it comes up when someone applies for a payday loan online. They want to know if our check is a “soft” hit or a “hard” hit.

First of all, there is often a bit of confusion between a credit report and a credit score. Your credit report is exactly what it sounds like – the full details of your credit history, including names of companies or banks who have provided you with one type of line of credit or another. Your credit report can be obtained for free (click here for full instructions). Your credit score, however, is the number that reflects your “credit worthiness”, so to speak. That number may or may not appear on your credit report, and most reporting agencies charge a modest fee to include it on your report.

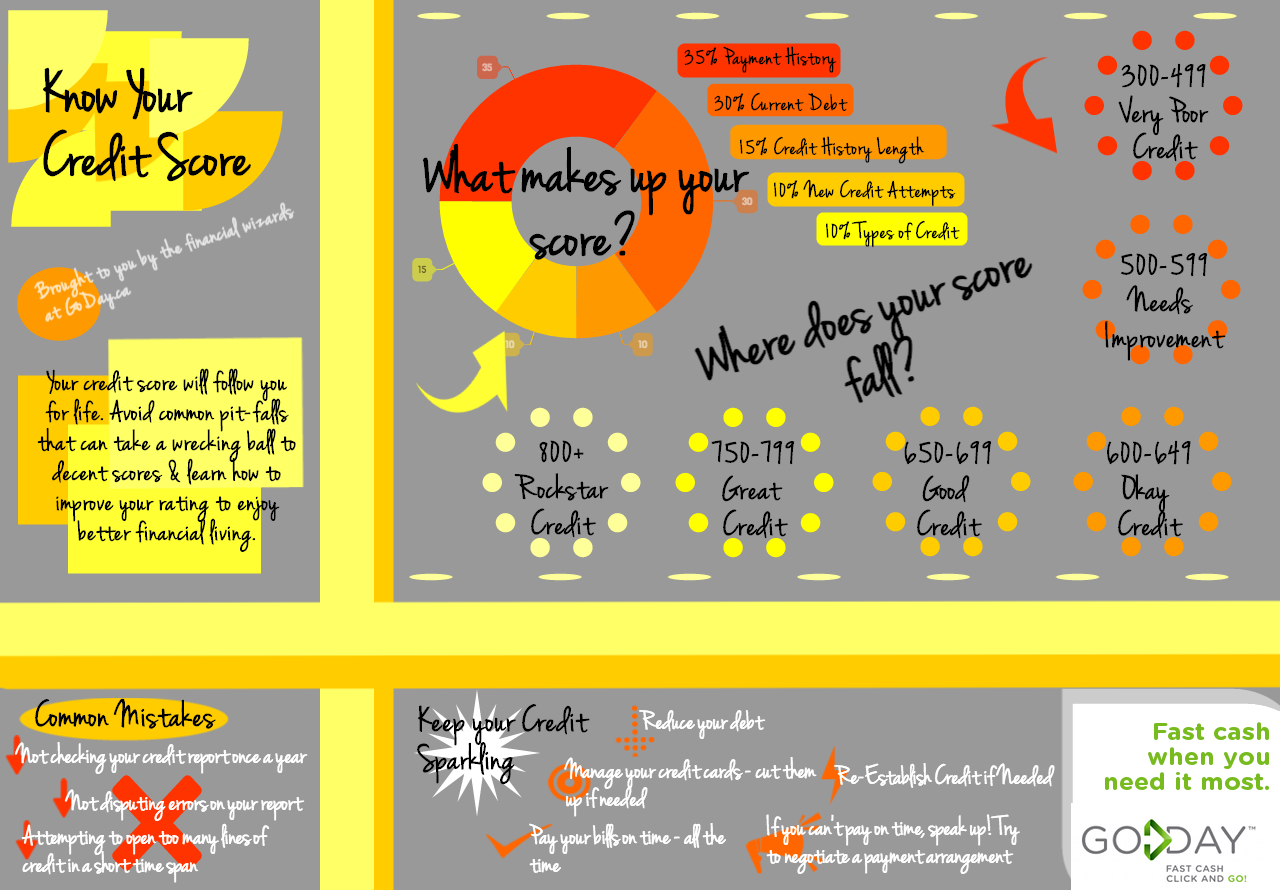

Knowing what’s in your credit history is important, especially with increasing stories of identity theft, so we recommend getting a free report at least once a year. Some people check up on it every 6 months. Talk to a financial advisor to discuss what’s best for you and your goals.

Secondly, in regards to “soft & hard hits”, there is a bit of confusion here, too. Any time a business “looks at” your credit history, it can be considered either a soft hit or a hard hit. A hard hit, or hard inquiry, is the only type of inquiry that actually affects your credit score and these hits are visible to other inquirers. Inquiries from credit card companies, rental companies, banks and possibly employers often count as a hard hit. A perfect example of a hard-hit is when you apply for a credit card or car loan. It also applies when you submit a request for an increase in credit.

A common mistake is to think that “rate shopping” for a car or mortgage are soft-hits, but this generally isn’t true, so if you’re in the market for a service or product that relies on credit, try to complete all of your “shopping” in a one to two week time frame, as they might be grouped together and treated as one inquiry. There’s no guarantee on this, however.

A “soft hit”, or soft inquiry, is the total opposite. Your credit isn’t being reviewed in the same manner it is during a hard hit. Soft hits do not impact your score in any way what-so-ever (as in, your the number that represents your credit worthiness will not be changed positively or negatively), the inquiry will just appear as another line on your report. Examples of a soft hit would be a business requesting your report to update the records that they might have on you (after you grant them permission, of course). Another example is when you request your own credit report.

Here’s to your credit health!

Want more knowledge? You might also like:

Direct Payday Loan Lenders VS Indirect Payday Loan Lenders

Payday Loan Industry Update: Cash Store Financial Services Inc. Ordered to Repay Fees to Customers

A Penny For These Thoughts: I got a Payday Loan